Fair value S$1.19

Good results to continue

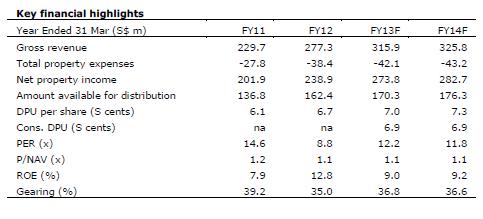

Mapletree Logistics Trust’s (MLT) financial performance for the trailing four quarters ending 31 Mar 2012 had been outstanding, buoyed by a slew of yield-accretive acquisitions and healthy organic growth from its existing portfolio. In the year ahead, we expect MLT to deliver again, as it continues to optimize its portfolio yield and invest in quality assets. YTD, we note that MLT has acquired close to S$390m worth of properties with initial NPI yields of 6.2-9.9%. The last of the announced acquisitions (Fuji warehouse and Celestica Hub in Malaysia) was completed in May, and is expected to contribute positively to its distributable income going forward.

In a sturdy financial position

As at 31 Mar, MLT’s aggregate leverage was at a comfortable 35.2% mark, bolstered by the issuance of S$350m perpetual securities and asset revaluation gain of S$113.0m (~3% increase). Even with the completion of all committed acquisitions, we estimate its gearing ratio to inch up to only ~37% - a level we deem is still healthy. Notably, its weighted average debt duration has also been extended from 2.2 years in prior year to 4.2 years as a result of management’s proactive capital management initiatives. Hence, we believe MLT is well positioned to pursue its growth strategy, with minimal refinancing baggage to carry through the coming year.

MLT’s unit price has also performed well, raking up a return of 17.2% YTD as opposed to 13.0% gain in the benchmark index. While the REIT was sold down by as much as 4.9% from its peak on 10 Jul, we note that it was due to a sale in Alliance Global Properties’ 5.7% stake in MLT via a block trade, and not a drastic change in its fundamentals. At current price, MLT still offers an attractive upside potential and respectable FY13F yield of 7.1%. We maintain our BUY rating on MLT, with a revised fair value of S$1.19 (S$1.20 previously) after finetuning our model to incorporate the exact acquisition completion dates.

No comments:

Post a Comment