Target Price S$2.58

What’s New

• We held a series of investor meetings with Olam International. Attendees from the company include Mr Shekhar Anatharaman, Executive Director – Finance and Business Development, as well as investor relations managers Mr Aditya Renjen and Ms Chow Hung Hoeng.

Key takeaways

• “Not a temporary role”. Shekhar’s appointment in his current role is not meant as a stop-gap measure to fill the role of CFO. His appointment was announced on 20 June, together with the resignation of CFO Ravi Kumar. (We hear Ravi is joining a Middle East telco.) Shekhar has been with the group since 1992 and has had oversight responsibility for the edible nuts, spices & vegetable ingredients (SVI) and packaged foods businesses. He also had the functional oversight of the Manufacturing and Technical Services (MATS) function and previously held senior roles in Country Management, as well as led various corporate functions like Finance, Treasury, and IT. Shekhar will perform his new role full-time and will be relieved of his duties overseeing the P&L of operational business units.

• Strategy unchanged, focus on risk management, FCF. Olam will continue to

focus on the execution of initiatives in its strategic plan, of which 60-70% has been initiated. While risk management has always been an important part of Olam, Shekhar indicated that he will place further emphasis on risk management in light of the volatile operating environment. In addition, he will seek to keep Olam on track in achieving a positive free cash flow within the next two FYs.

• IRM segment guidance unchanged. Guidance from the 3QFY12 results announcement that there would be continued weakness in the industrial raw materials (IRM) segment remains unchanged. Specifically, cotton could see a couple of quarters more weakness as Australian farmers continue to defer volumes in anticipation of better prices.

• However, volumes could come through by 2QFY13 as warehouses have to be cleared out for the next cotton crop. The wood products business is also not likely to see an immediate upturn as demand from the construction and furniture industries is still weak.

• Rationale for share buyback. The buyback of shares in the past month reflects the Olam Board’s view that the stock price was trading significantly below its intrinsic value, even to a point where returns were attractive in comparison to the universe of opportunities available to the group.

• Balance sheet is robust and well-positioned to execute strategic plan. Olam has actively managed its financing needs to better match changes and anticipated changes to its asset structure, ie having a higher proportion of fixed assets. Olam’s sources of debt are increasingly diversified, including a mix of bilateral and syndicated debt, and tapping from a variety of debt capital markets. Debt maturities have also been extended to spread out liquidity requirements. It was re-iterated that the execution of the group’s strategic plan for FY16 required no further equity raising.

• Gabon project on track. Olam’s Gabon fertiliser project is on track for commencement in 1Q15.

Stock Impact

• Short-term earnings weakness could dampen interest, but watch out for rebound in IRM. If Olam is able to demonstrate continued resilience in its food-based segments in the next two quarters and barring any major dislocations in financial markets, we believe the stock could re-rate upwards on resumption of earnings growth.

Earnings Revision/Risk

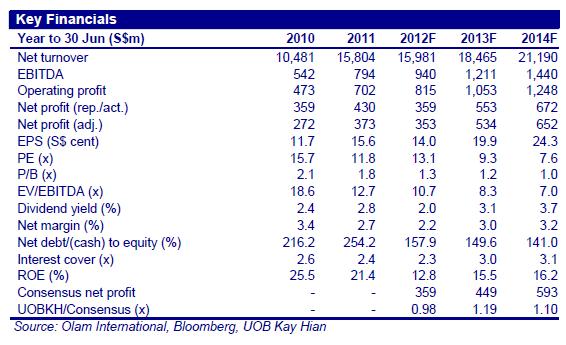

• No changes to our earnings estimate. We expect margin expansion in FY13 due to more stable cotton prices and a deferment of cotton volumes from FY12. Key risks include lower-than-expected volume growth, execution risks for initiatives in progress.

Valuation/Recommendation

• Maintain BUY. We maintain our target price of S$2.58, based on 15x FY12/FY13 average earnings.

No comments:

Post a Comment