• FY11 net profit of S$527m was slightly above; higher final DPS of 12.5Scts (FY10: 11.5Scts)

• Record S$12.3bn orderbook provides good visibility, but growth is unexciting

• Maintain HOLD with higher TP of S$3.25

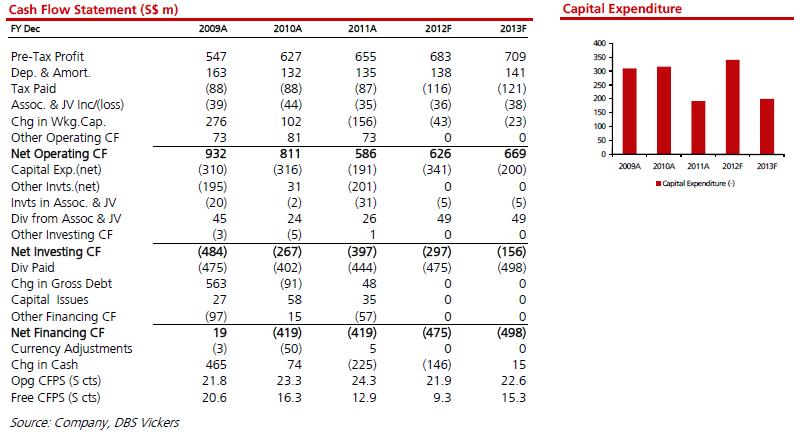

Stronger US$ in 4Q, better results. STE reported betterthan- expected results in 4Q11, driven by higher revenues and better margins in a stronger US$ environment. 4Q11 net profit was up 6% y-o-y to S$152m, driving FY11 net profit up 7% yo- y to S$528m. All segments recorded revenue growth in 4Q11 except Marine due to the Ropax ferry contract termination. PBT was driven by better sales mix at Land Systems and Marine sectors. Aerospace PBT margin was strong at 14% in 4Q11. Group PBT was up 4% in FY11 but lower effective tax rate contributed to the higher net profit growth. FY11 growth was decent although US$ weakened by almost S$0.10 on average against S$.

The Group ended the year with a record S$12.3bn orderbook, which ensures steady revenue growth and earnings delivery, going forward. Management outlined its growth strategy through acquisitions (e.g. Nera Tel), new facilities like the Xiamen engine center and the upcoming MRO facility at Guangzhou, new capabilities like VIP aircraft interior modification, and expansion of existing facilities like building more capacity at Seletar Aerospace Park in Singapore and adding a shiprepair business at VT Halter Marine’s yards in the US. However, other than any big acquisitions, we believe other growth plans are more medium term in nature.

Healthy yield is the key attraction. We raise our FY12-13 EPS estimates by 3-4% to reflect the better-than-expected results. However, STE’s significant exposure to sluggish US/EU economies could cap its growth potential in FY12. Maintain HOLD on the stock for its strong balance sheet (net cash of S$405m) and yield in excess of 5%. Raise TP to S$3.25 in line with earnings revision.

Click Picture To Enlarge

ST Engineering – FY11 results review Group

Group

+ FY11 revenue of S$5,991m came in flat, while PBT was up 4% y-o-y

+ Excluding the impact of weak US$, revenue is estimated to be higher by S$184m Aerospace

Aerospace+ Revenue of S$1,927m was up 3% y-o-y, driven by more engine inputs in Component/ Engine Repair division and milestone completions in Engineering & Material Services business group

+ Heavy maintenance division was impacted by weaker US$ owing to translation losses

+ PBT of S$278m was up 6% y-o-y, partly driven by revision of inventory obsolescence estimates in FY11.

+ Core PBT margins remained strong at around 14% Electronics

Electronic+ Revenue was up 6% to S$1,517m, as all business lines recorded higher sales, including milestone completions of LTA’s Circle Line project in Singapore, the half height platform doors project in Singapore and Bangkok automatic fare collection systems

+ PBT margins inched up slightly to 9% owing to favourable sales mix in Large Scale Systems business, thus resulting in 7% growth in PBT for FY11 Land Systems

Land Systems+ Revenue of S$1,506m was comparable y-o-y, as lower sales in Munitions & Weapon segment was offset by higher sales in Automotive and Trading segments

+ PBT was down 5% in FY11, owing to lower margins in the M&W segment

+ Automotive segment margins were better though in FY11, as the Group finished deliveries of the lowermargin Bronco armoured vehicle to the UK Army earlier in the year Marine

Marine+ Revenue of S$877m was down 16% y-o-y owing to the reversal of S$176m revenue recognised from the Ropax ferry contract, which was terminated in FY11.

+ Excluding this, revenue would have been flat, as higher shiprepair activities offset lower shipbuilding revenues

+ PBT was up by 3%, as margins improved significantly for the shipbuilding business, likely at its US shipyard, VT Halter Marine

Click here for ST Engg 50/200MA + Volume + MACD + RSI

No comments:

Post a Comment