Target price - S$0.72

What’s the fuss all about? Cosco simply looks overvalued. While the market has grown more optimistic about the marine sector on account of a few key contract wins by the established offshore yards, Cosco still does not have the credentials or the fundamentals to ride those coattails. Its recently-reported FY11 financials also do not inspire confidence. We maintain our Sell recommendation on Cosco and maintain our target price at $0.72.

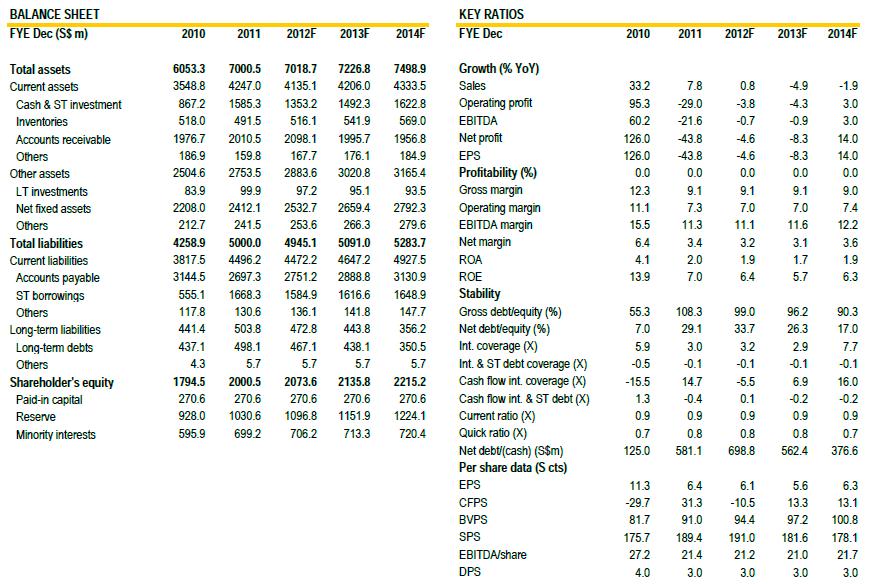

Numbers are down and will stay down. While Cosco’s FY11 net profit decline of 44% to $139.7m despite an 8% pickup in revenue came as no particular surprise to the market, its share price has been resilient and valuations have stayed rich. However, we believe that market optimism on the stock is misplaced, as we see no recovery to its earnings based on its current orderbook and our projection of new order wins. Core margins remain weak, hovering at an abysmal 2.8%.

Financials still problematic. Cosco’s financial metrics continue to be weak across the board. Gearing, for one, has jumped from 7% in FY10 to 29% at end-FY11 after the company increased borrowings to expand its yards and finance its ongoing orders. In addition, provisions are still being made for its ongoing jobs due to start-up and execution issues, particularly with regard to the more complex offshore jobs.

Orderbook not growing. With a recent US$190m order win for the bulk carrier segment unexciting, net orderbook now stands at US$6.2b. This is still lower than its peak of US$7.0b at June 2011. US$300m in new orders have been secured year-to-date. This is still running short of management’s expectation to secure some US$2b in orders for FY12. Furthermore, the quality of new orders remains in question, with weak pricing for bulkers, and a risk to margins for potential offshore wins.

Premium unjustified, maintain Sell. With peers trading at a PER of 12x, we see no reason for Cosco to trade at a premium in view of its declining EPS. A re-rating to its peers values Cosco at $0.72, or downside of 39.7%, hence our Sell call.

Financial and operating data hardly inspiring

Money for nothing. Cosco’s net gearing has risen to 29% in FY11 from 7% a year ago, as the company sought to finance its shipyard activities’ working capital and yard expansion. But it still has some $1.6b cash sitting in its books. This money is made up of customer deposits and $1.2b of cash raised through bank borrowings. These funds will be progressively deployed through the year as working capital as the company converts on its orderbook. This is because most of the offshore projects have been secured on 20/80 payment terms, whereby Cosco will have to fund the bulk of the working capital upfront and only collect cash payment on completion and delivery to the customer. Gearing is thus set to grow over the course of the year. As it is, gross gearing stands at a distressing 108%. So, besides exposing itself to cash flow risk in the event of a default by the customer, even a successful delivery at the current margins seems like a lot of effort with very little return.

Core margins razor thin. Figure 1 illustrates the extent to which Cosco’s operating margins have fallen as a result of lower pricing for its newbuilds and cost overruns on its offshore projects. We estimate that EBIT margins reported for both bulk carrier newbuilds and offshore are hovering at 3-4%, while ship repair is relatively healthy at about 12%. However, Cosco’s earnings have always been boosted by scrap material sales from discarded steel used in its ship repair and shipbuilding processes. In FY11, the company recorded a $95.2m gain from this, which makes up a very significant percentage of its EBIT of $305.2m. In addition, it enjoyed a net currency exchange gain of $50.6m during the year. Stripping these items out, core EBIT margins stood at just 2.8%.

Whatever margin is left can very quickly be eroded by an appreciation of the RMB, rising interest rates in China, higher wages and firmer raw material prices (steel in particular). Hence, we see high risk to our muted earnings forecast.

Bulk carrier newbuild margins under pressure. Currently, Cosco has an outstanding orderbook of about US$6.4b, which comprises mainly 53 bulk carriers ranging from 35,000dwt to 92,000dwt. On its books are also four special carriers. The company intends to deliver 37 of these in the current year and this will leave quite a significant gap in its yard capacity, unless there is a resurgence of orders.

However, we note that the pricing of bulk carrier newbuilds continues to be extremely weak. This is in line with the low market demand for such vessels, as evidenced by the declining charter rates pushing the Baltic Dry Index to rock bottom (Figure 2). Any new orders are likely to come at the further expense of margins. Although Cosco believes that it may achieve cost savings from improved productivity and efficiency gains, management does concede that shipbuilding margins will continue to languish in FY12.

Bulk carrier fleet barely at breakeven. Cosco continues to run a fleet of 10 dry bulk carriers, most of which are operated on spot contracts. As a result, bulk shipping barely broke even over the past six quarters. The current Baltic Dry Index shows that rates remain weak, and we do not expect this segment of Cosco’s business to recover anytime soon.

Diverse offshore job portfolio defeats efficiency. On the offshore front, Cosco’s portfolio of newbuild contracts is extremely diverse. This makes it difficult for the company to achieve economies of scale and build efficiencies since each job specification is different. We think Cosco may be sacrificing its margin in order to build up expertise in these various areas. The vessels under construction include:

- 1 deepwater drill ship

- 1 wind turbine installation vessel

- 3 Sevan Marine cylindrical drilling units

- 3 tender rigs

- 2 semisubmersible vessels

- 2 pipelay vessels

- 2 jack-up rigs

- 1 semisubmersible barge

Order flow trailing off. With just US$300m in new orders secured year-to-date, this is behind the run rate of new orders Cosco won in previous years. In 2010, the company snared US$1.9b in new orders and topped this with US$2b worth of orders the following year, of which 95% came from the offshore segment. We note that order flows tend to be choppy and lumpy. A surge of new orders may well come in over the course of the year. For now, we would rather remain conservative and expect no more than US$1.2b worth of orders, versus management’s expectation of US$2b.

No pickup in earnings, premium unjustified. We anticipate flat earnings growth for Cosco over the next two years, given its shrinking orderbook and thin margins. Therefore, we see no justification why the stock should trade at a significant premium over the sector. Established shipyards such as Keppel Corp and Sembcorp Marine are only trading at 12.8x and 14.8x forward PER, respectively – and with much better earnings and new order prospects. They also have an outstanding track record for execution. The overall sector trades at a mean of 12x PER, which is where we peg our FY12 earnings multiple, hence our target price of $0.72 per share for Cosco. We also warn, as above, of the potential risk to Cosco’s earnings. Maintain Sell.

No comments:

Post a Comment