Results

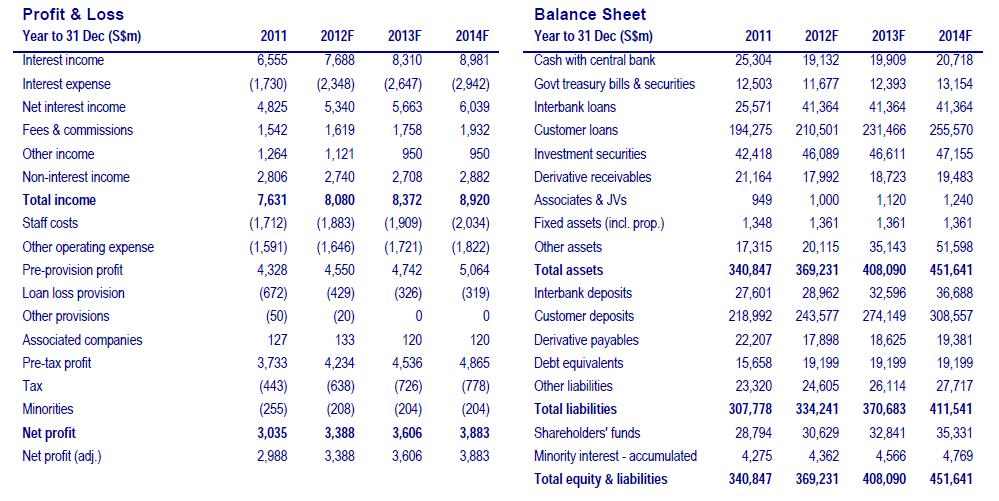

- DBS reported a net profit of S$856m (+6% qoq, +12% yoy) for 3Q12, above our forecast of S$799m and consensus estimate of S$801m.

- Slowdown in loans from North Asia. Loans contracted 1.3% qoq but increased

9.1% yoy. The sequential decline was due to Hong Kong (- 5.1% qoq) and China (-10.7% qoq). NIM contracted 5bp on a sequential basis to 1.67% as DBS collected more deposits and lowered its loan-todeposit ratio (LDR) from 89% to 84.3%. Deposits expanded 4.2% qoq with US dollar deposits growing by a hefty 10.9% qoq.

- Growth from non-interest income. Net fee income grew 11% qoq to S$422m. Contribution from investment banking was significant at S$60m due to the IPOs for IHH Healthcare, Far East Hospitality Trust and Ascendas Hospitality Trust. Net trading income remains below par at S$137m, which we have already anticipated. DBS also recognised an income of S$110m from financial investments.

- Balance sheet strengthened. NPL ratio remains unchanged at 1.3%. Total provisions dropped from S$104m in 2Q12 to S$55m in 3Q12. Loan loss coverage improved from 129% to 134% as non-performing loans (NPL) declined by 4.1% qoq. Core equity tier-1 (CET-1) CAR also improved from 11% to 11.6%. Book value per share (BVPS) increased 1.1% qoq to S$12.50.

- DBS has clocked 11 quarters of consistently strong financial performance under new CEO Piyush Gupta, reflecting excellence in execution as well as a wining management team at DBS.

- We see 3Q12 results as broadly in line with our expectations.

- DBS provides attractive valuation with P/B at 1.1x and dividend yield at 4.1%. It was able to generate growth in earnings despite macro headwinds due to growth in fee income and lower credit costs

Earnings Revision/Risk

- We have fine-tuned our earnings forecast, which remains relatively unchanged.

Valuation/Recommendation

- We have rolled forward our valuation to 2013. Our target price for DBS is S$20.80 based on P/B ratio of 1.55x, which is derived from the Gordon Growth Model (ROE: 11.4%, required return: 8.0% and constant growth: 1.8%).

Share Price Catalyst

- Organic growth from the global transaction service, wealth management and SME businesses, which are also the regional businesses earmarked in its nine strategic priorities.

- Growth prospects enhanced with greater contribution from high-growth emerging markets if DBS successfully acquires Bank Danamon.

It's important to note that the relationship between loans and the balance sheet is complex, and there could be other factors at play. The "strengthened balance sheet" generally indicates positive financial management, but the exact implications depend on the company's specific circumstances, industry trends, and broader economic conditions. If you're referring to a specific company or situation, more context would be needed to provide a more accurate assessment. Business cashflow forecasting software | Financial Management for SMEs

ReplyDelete